PEO Governance: Warnings and The Missing Discipline in Co-Employment Relationships

Post 4 of the PEO Governance Series

A PEO relationship does not fail on a single day. It drifts. How to see the warning signs

- → Slowly. Quietly. Over months.

- → And by the time leadership notices, the correction is expensive.

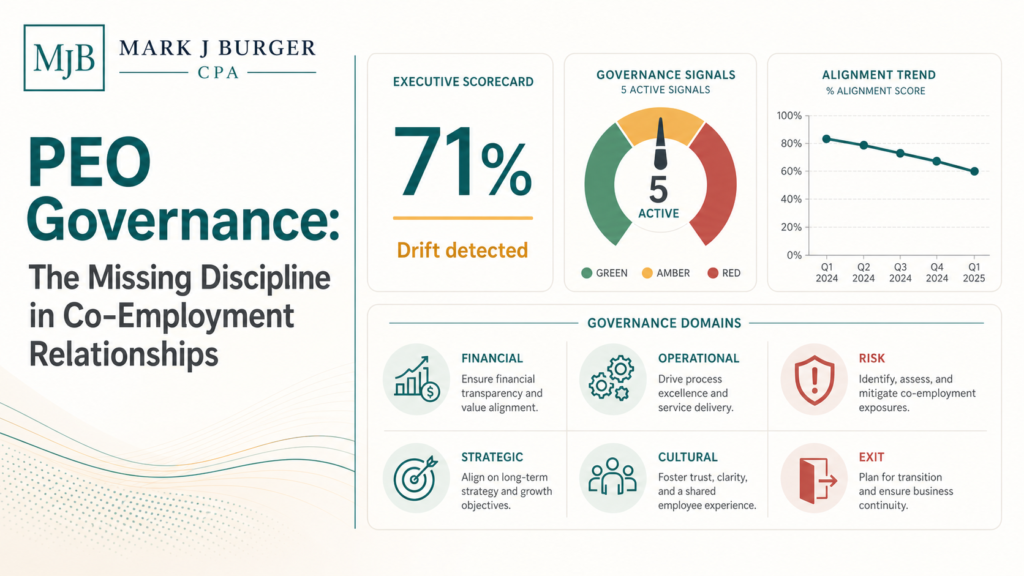

In the first three posts of this series, we established the governance discipline, identified the six domains where oversight must live, and delivered a practical framework — the PEO Alignment Monitoring System — with quarterly dashboards, traffic light scoring, and defined escalation triggers.

But frameworks require one thing to function: the ability to recognize when something is wrong.

Misalignment shows up six to eighteen months before most owners recognize it.

The signals are there. They surface in operational patterns, financial trends, team behaviors, and leadership assumptions. They are rarely dramatic. They do not arrive as crises. They arrive as small, easily dismissed observations that accumulate until a triggering event — a renewal increase, a compliance failure, a key employee departure — forces the conversation that should have happened three quarters earlier.

This post identifies the twelve most common early warning signs we observe across PEO-client relationships. Each one maps back to a specific governance domain from the framework. Each one is detectable if someone is watching.

The question is whether anyone in your organization is watching.

The Twelve Warning Signs

Warning Sign 1: Reviews Only Happen at Renewal

This is the single most common governance failure in PEO relationships. The contract is signed. Onboarding is completed. And the next structured conversation about the relationship occurs twelve months later when the renewal proposal arrives.

Twelve months of invoices paid without dissection. Twelve months of claims data unreported. Twelve months of service quality unexamined. And now the business is expected to evaluate a renewal increase with no baseline data, no trend analysis, and no leverage.

If the only time your leadership team discusses the PEO relationship is when the renewal invoice arrives, governance does not exist. You are reacting to outcomes rather than managing the inputs that created them.

Governance Domain: Financial Governance, Strategic Alignment

Warning Sign 2: The Relationship Is Managed Too Far Down the Organization

A PEO is not a vendor that delivers supplies. It is a co-employer that touches payroll, benefits, compliance, workers’ compensation, and employee relations. The strategic implications of that relationship demand executive-level attention.

When the PEO relationship is managed exclusively by an office manager, a bookkeeper, or a junior HR coordinator, the signals that matter — cost trends, risk exposure shifts, strategic misalignment — never reach the people with authority to act on them. The person managing the relationship may be excellent at day-to-day coordination but lacks the organizational context to recognize when the PEO model is falling out of alignment with the company’s direction.

The PEO relationship should report into an executive who owns the governance cadence. Anything less is delegation without oversight.

Governance Domain: Strategic Alignment, Operational Governance

Warning Sign 3: Invoices Are Not Reconciled Thoroughly

A PEO invoice is a composite of multiple cost components: administrative fees, benefits premiums, workers’ compensation charges, payroll taxes, and technology fees. Each component moves independently. Each one can increase without triggering a visible alert. Industry data confirms that PEO administrative fees range from $40 to $160 per employee per month, or two to six percent of payroll — but the quoted rate is rarely the actual cost. Hidden fees for off-cycle payroll runs, COBRA administration, termination processing, and year-end W-2 preparation compound across a year without appearing in the original proposal.

Most businesses pay the total. Few dissect the components. Fewer still track those components over time to identify trends. And almost none compare those trends against revenue, headcount, and claims data to determine whether the cost trajectory is justified.

If your finance team processes the PEO invoice the same way it processes a utility bill — pay the total, file the receipt — cost drift is not a risk. It is a certainty.

Governance Domain: Financial Governance

2026 Context: The One Big Beautiful Bill Act’s new payroll withholding rules and the Secure 2.0 Roth catch-up mandate have introduced additional invoice line items and tax treatment changes effective 2026. If your finance team is not reviewing invoices at the component level, these regulatory changes may be implemented incorrectly without anyone noticing.

Warning Sign 4: Claims Data Is Not Analyzed

Workers’ compensation claims data is one of the most powerful governance tools available to a PEO client. It reveals patterns in workplace safety, identifies high-risk departments or locations, and directly influences the experience modification rate that drives premium costs. Your experience modification rate is the single largest variable in your workers’ compensation premium. A mod of 1.25 means you are paying 25 percent above the standard rate for your classification — and even minor issues such as misclassifications, delayed claims management, or inconsistent safety practices can materially impact that number at renewal.

Most businesses receive claims reports. Few analyze them. The report sits in a file or an inbox. No one asks whether claims frequency is increasing, whether severity is trending upward, whether specific locations or departments are driving disproportionate activity, or whether the PEO’s safety programs are having any measurable impact.

Unanalyzed claims data is not data. It is noise. And noise does not prevent the premium increase that arrives at renewal.

Governance Domain: Risk Governance, Financial Governance

Warning Sign 5: Service Team Turnover Increases

The quality of a PEO relationship is built on the people who deliver the service. When a dedicated service representative leaves and is replaced by a shared team, or when the assigned representative changes multiple times in a twelve-month period, continuity of knowledge erodes.

The new representative does not know your company’s history, your specific compliance requirements, your benefits selection rationale, or the informal agreements that shaped the relationship. Every transition resets the learning curve. And each reset degrades the responsiveness, accuracy, and contextual awareness that defined the service at onboarding.

If you have had more than one service team change in a year and no one at the executive level discussed it with the PEO, operational governance is absent.

Governance Domain: Operational Governance

Warning Sign 6: Payroll Errors Rise

A single payroll error is a mistake. A second payroll error is a concern. A pattern of payroll errors is a system failure.

Payroll accuracy is the most visible measure of PEO operational quality because employees notice immediately. Incorrect withholdings, missed deductions, late deposits, and tax filing errors erode employee trust and create compliance exposure for the employer.

The governance question is not whether an error occurred. It is whether the error rate is trending upward over time, and if so, whether the root cause is staffing, technology, volume, or a combination. Without tracking, a rising error rate looks like a series of isolated incidents rather than the systemic degradation it actually represents.

Governance Domain: Operational Governance

2026 Context: The implementation of new withholding mechanics under the One Big Beautiful Bill Act and PFML payroll tax changes across expanding state programs creates additional processing complexity for PEOs in 2026. A payroll error rate that was stable in 2024 may begin climbing as these new requirements take effect. Your Operational Dashboard should be tracking whether errors correlate with regulatory implementation timelines.

Warning Sign 7: Hiring Friction Increases

A PEO should accelerate the hiring process, not slow it down. When onboarding new employees becomes cumbersome, when benefits enrollment creates confusion, when managers report that the hiring experience is creating a poor first impression, the PEO model is generating friction rather than reducing it.

Hiring friction is a strategic alignment signal. It means the PEO’s onboarding infrastructure, benefits platform, or enrollment processes are not keeping pace with the company’s hiring velocity or the expectations of the candidates being recruited.

In a labor market where first impressions matter, a clumsy onboarding experience does not just frustrate managers. It costs talent. Research from the Society for Human Resource Management estimates that replacing a single employee costs 50 to 200 percent of their annual salary, and the average time to fill a position is 44 days. For a 20-person team losing just two employees per year, the hidden cost of turnover can reach $100,000 to $400,000 annually. When the PEO’s onboarding process is contributing to that friction rather than reducing it, the cost is not theoretical. It is measurable.

Governance Domain: Strategic Alignment, Operational Governance

Warning Sign 8: Renewal Increases Are Accepted Without Modeling

A PEO renewal proposal is not a final offer. It is a starting point for a data-driven conversation. But that conversation requires data — twelve months of tracked cost components, claims trends, service metrics, and market benchmarks.

When a business accepts a renewal increase without modeling the components that drove it, without comparing the increase to industry benchmarks, and without negotiating the terms, the PEO has no reason to sharpen its pricing. The client has signaled that cost is not being monitored.

Renewal acceptance without modeling is not just a financial governance failure. It is a signal to the PEO that governance does not exist — and that signal influences every future renewal.

Governance Domain: Financial Governance, Exit and Contingency Governance

Warning Sign 9: Managers Bypass HR Processes

When managers stop using the PEO’s HR tools, stop following documented discipline procedures, or begin handling employee issues directly without engaging the PEO’s HR team, the co-employment model is breaking down at the operational level.

Bypass behavior has two causes. Either the PEO’s processes are too slow, too cumbersome, or too unresponsive — which is an operational governance failure. Or managers do not understand their role in the co-employment structure — which is a cultural governance failure.

Either way, bypass behavior creates liability. Disciplinary actions taken without proper documentation, investigations conducted without HR involvement, and terminations executed without compliance review expose the company to employment claims that the PEO relationship was designed to prevent.

Governance Domain: Cultural Governance, Operational Governance, Risk Governance

Warning Sign 10: No Exit Strategy Exists

Every PEO relationship should operate with the assumption that it may not be permanent. Companies grow beyond the PEO model. Service quality declines. Better-aligned providers emerge. Strategic needs change.

If your leadership team does not know the contractual notice requirements for termination, does not have a data portability plan, does not understand the financial implications of transition, and has not identified what internal capabilities would need to be built or sourced to operate independently — exit governance does not exist.

The absence of an exit strategy does not mean the company will never need to leave. It means the company will be unprepared when it does. And unprepared transitions are the most expensive, most disruptive, and most damaging to employee trust.

Governance Domain: Exit and Contingency Governance

Warning Sign 11: Growth Into New States Feels Complicated

A PEO is supposed to simplify multi-state employment. That is one of the primary reasons businesses enter the relationship. When expansion into a new jurisdiction creates confusion about tax obligations, benefits requirements, employment law compliance, or registration timelines, the PEO model is not delivering on one of its core promises.

Multi-state complexity is increasing, not decreasing. Each state carries its own wage and hour laws, paid leave mandates, tax structures, and employment regulations. A PEO that was adequate for single-state operations may lack the infrastructure, expertise, or responsiveness to support a company expanding across multiple jurisdictions.

If growth is being delayed, complicated, or constrained by the PEO relationship rather than enabled by it, strategic alignment has failed.

Governance Domain: Strategic Alignment

2026 Context: With paid family and medical leave programs now enacted in 14 jurisdictions and Oregon’s HB 2236 introducing PEO client-by-client state tax reporting elections for 2026, multi-state complexity is accelerating. State-level AI employment regulations are adding another layer of compliance variability. If your PEO is struggling to keep pace with the regulatory landscape across your current footprint, expansion into additional states will amplify every existing gap.

Warning Sign 12: Leadership Says, “It Is Probably Fine”

This is the most dangerous warning sign on the list. Not because the words themselves are harmful, but because of what they reveal: the complete absence of data-driven confidence.

“It is probably fine” is not an assessment. It is an assumption. It means no one has reviewed the financial trends, examined the claims data, evaluated service quality, tested strategic alignment, audited cultural clarity, or confirmed exit readiness. It means every governance domain is operating on hope rather than evidence.

When leadership expresses confidence in the PEO relationship without being able to cite specific data points, metrics, or recent review findings, the confidence is not real. It is comfort. And comfort is the most expensive form of neglect in a co-employment relationship.

Governance Domain: All Six Governance Domains

Why These Signals Are More Urgent in 2026

Every one of these twelve warning signs exists in any year. But the 2025-2026 regulatory environment has intensified the consequences of ignoring them.

- The One Big Beautiful Bill Act introduced new payroll withholding mechanics for tips and overtime, effective January 1, 2026, adding processing complexity to every PEO invoice.

- Secure 2.0 mandates Roth-only catch-up contributions for highly compensated employees, with IRS proposed regulations directly addressing the Certified PEO relationship.

- Paid family and medical leave programs have now been enacted in 14 jurisdictions, with Oregon’s HB 2236 creating new PEO client-by-client reporting elections for 2026.

- IRS Revenue Ruling 2025-4 reclassified employer pickup contributions of PFML premiums as wages subject to federal income and employment taxes, creating new reporting obligations.

- Multiple states have enacted or proposed laws regulating AI in employment decisions, requiring transparency, bias testing, and recordkeeping — directly impacting PEOs that use AI-driven hiring and HR tools.

- OSHA serious violation penalties now reach $16,550 per incident, with willful violations at $165,514 — making risk governance failures exponentially more expensive.

Each of these regulatory changes creates new compliance requirements, new invoice components, and new points of potential failure within the PEO relationship. A business that is not monitoring for the twelve warning signs in this post is not just drifting. It is drifting into a regulatory environment that penalizes the absence of governance more severely than at any point in the past decade.

Learn more: The Ultimate PEO Integration Guide That Saves You From Hidden Costs

The research supports the urgency. NAPEO data indicates that organizations partnering with PEOs can achieve roughly 27 percent total cost savings across HR-related areas — but only when the relationship is actively managed. PEO clients that do not govern the relationship forfeit those savings incrementally, through hidden fee accumulation, unexamined renewal increases, and compliance exposure that no one detected until it became a financial event.

Connecting the Signals to the System

None of these twelve warning signs exist in isolation. They compound. A business that only reviews at renewal is also likely accepting renewal increases without modeling. A company where managers bypass HR processes is also likely experiencing rising payroll errors. An organization without an exit strategy is also likely managed too far down the org chart.

Drift is not twelve separate problems. It is one problem expressing itself across twelve dimensions.

The PEO Alignment Monitoring System introduced in Post 3 of this series was designed to detect these signals before they become consequences. The quarterly dashboards surface the data. The traffic light scoring creates accountability. The escalation triggers create decisiveness. And the Original Intent Document provides the reference point against which every signal is measured.

The twelve warning signs in this post are the symptoms. The governance framework is the diagnostic system. Together, they transform passive outsourcing into active management.

The Question That Matters

Every business owner reading this list recognizes at least two or three of these warning signs in their own organization. That recognition is not failure. It is the beginning of governance.

- Recognizing drift is the first step.

- Measuring drift is the second.

- Acting on what the measurement reveals is where governance lives.

Drift is subtle. Governance makes it visible.

The companies that practice this discipline do not experience renewal shock, compliance surprises, or the slow realization that their PEO model stopped serving them two years ago. They detect the signals. They act on the data. And they maintain a co-employment relationship that compounds value rather than hidden cost.

The most expensive sentence in business is “It is probably fine.” The second most expensive is “We will look at it at renewal.” Both share the same root cause: the absence of a system that makes drift visible before it becomes consequence.

Coming Next: In the final post of this series, we will address a critical question: how does an independent CPA advisor provide governance value in a PEO relationship? We will examine the role of objective financial analysis, compliance oversight, and strategic counsel in maintaining a co-employment relationship that serves the employer — not the other way around. Learn more about Mark J Burger CPA

Explore our full PEO advisory resources: PEOAdvisor.com or Start your free PEO Assessment: https://peoadvisor.com/assessment/

- What is this actually costing me in dollars right now — and how much worse does it get if I do nothing? The cost of ungoverned drift is specific and calculable. Industry data shows that PEO administrative fees range from $40 to $160 per employee per month, or two to six percent of payroll — but hidden fees for off-cycle payroll runs, COBRA administration, termination processing, and year-end adjustments compound across a year without appearing in the original proposal. Some PEOs apply a markup of five to twenty percent on health insurance premiums, and that markup is rarely transparent. For a 30-person company, total PEO costs typically fall between $18,000 and $46,800 annually before benefits pass-through and year-end adjustments — and that figure assumes every component is being monitored. When it is not, renewal increases of 15 to 25 percent become the norm rather than the exception, because the client has no historical data to challenge the proposal. Add the turnover cost — SHRM estimates replacement at 50 to 200 percent of annual salary per employee — and a 50-person company losing three employees per year to benefits misalignment or onboarding friction is absorbing $75,000 to $300,000 in hidden cost that governance would have surfaced quarters earlier. The compounding effect is what makes inaction so expensive. Each quarter of unmonitored drift narrows the options available at renewal and increases the cost of correction.

- How do I know which of these warning signs are actually happening in my business right now?” Start with one exercise. Ask your finance team to explain what changed in last month’s PEO invoice compared to the month before — not the total, but the components. Ask your operations leader whether payroll error frequency has increased over the past two quarters. Ask your HR contact when the last service representative change occurred and whether it was discussed at the executive level. If any of these questions produce hesitation, uncertainty, or silence, you have confirmed that at least three warning signs on this list are active. The PEO Alignment Monitoring System introduced in Post 3 of this series provides the structured diagnostic — three quarterly dashboards covering financial, risk, and operational metrics, with traffic light scoring that transforms uncertainty into measurable data. You do not need to monitor all twelve warning signs simultaneously. Start with the Financial Dashboard. If your team cannot populate it from existing PEO reports, that single finding tells you more about your governance posture than any checklist ever will.

- Who in my organization should own this, and what do I do first? Governance requires ownership, not committees. Assign one executive as the PEO governance owner — typically the CFO, COO, or the most senior leader who touches both finance and operations. That person does not need to do the analysis personally. They need to own the cadence and ensure it happens. Then assign domain responsibility: finance owns the Financial Dashboard, HR and legal own risk and cultural governance, operations owns the Operational Dashboard, and the CEO or COO owns strategic alignment and exit governance. All of them report into a single quarterly review meeting using the six domains as the standing agenda. The first concrete step is the simplest one in the entire framework: write the Original Intent Document. One page. Three questions. Why did we enter this PEO relationship? What must it deliver? What would trigger reconsideration? If that document does not exist today, nothing else in the governance system has a reference point. Start there. Schedule the first quarterly review within 30 days. Request the data from your PEO to populate the three dashboards. And if you want independent, objective guidance through that process, that is precisely the role an independent CPA advisor serves — which we will address in the final post of this series.